Update: Mastercard

Why I just doubled down on the payment giant.

Mastercard was previously one of my smaller holdings. In a market dominated by AI hype, when every company connected to AI seems to be shooting up 20% every other day, it might be surprising to hear that Mastercard, a relatively boring credit card company is my choice to invest serious money into. In today’s market, Mastercard seems… stale.

I believe that the way I view the stock is fundamentally different from the way the market views it. The market views Mastercard as a toll booth, I view it as a security infrastructure.

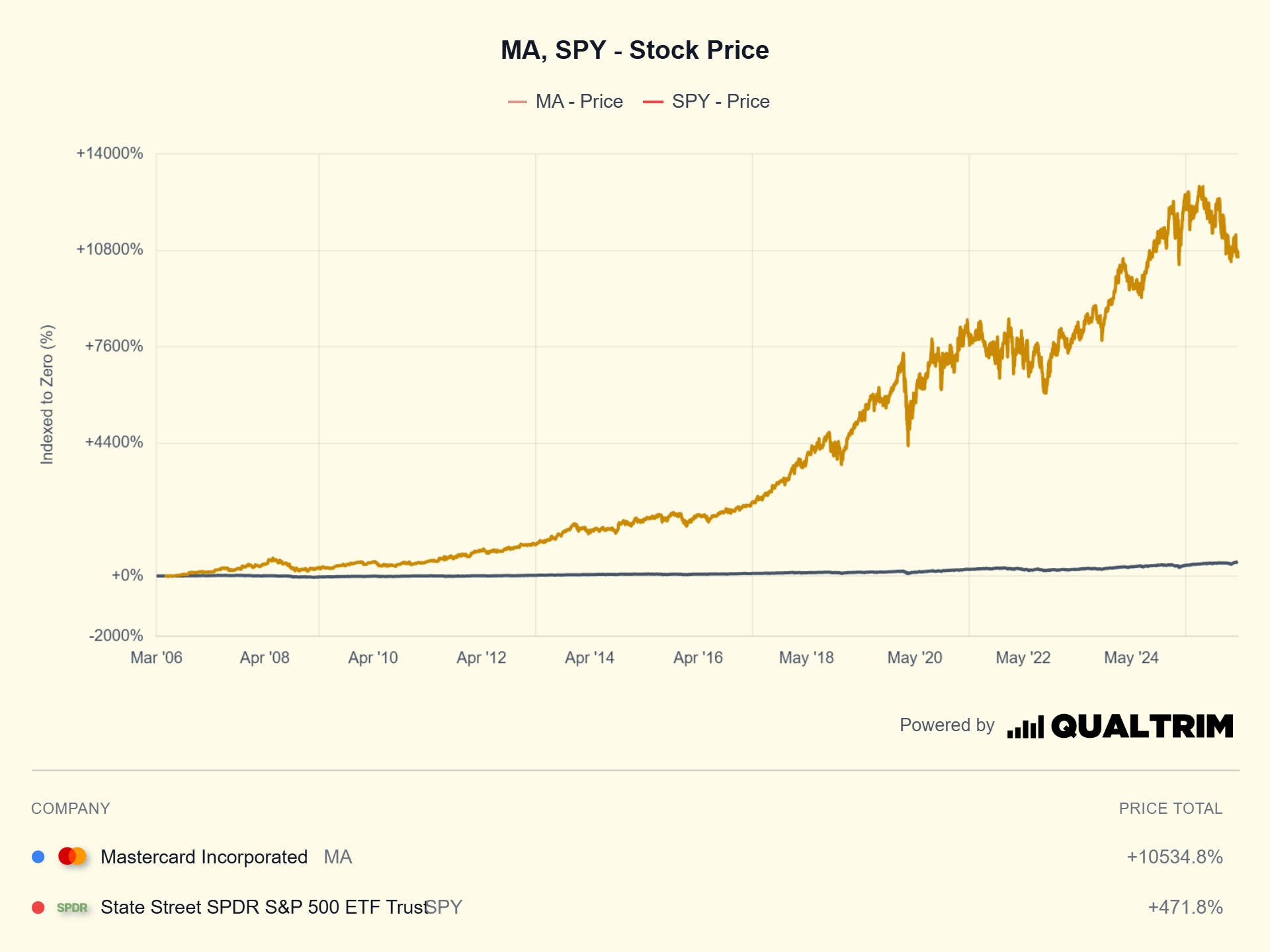

Boring companies might not be interesting, but some significantly outperform the market. Including Mastercard. A comparison of Mastercard and the S&P in the last twenty years looks almost comical. The S&P seems flat in comparison. Even in the last ten years, when Mastercard was already a dominant payment giant, it outperformed the S&P significantly. The S&P is up 260% in the last decade. Mastercard is up 410%. Costco is another good example of this, easily outperforming both Mastercard and the S&P over the last decade.

My initial post on Mastercard was posted while having about a 2% holding in Mastercard. I have decided now to invest another 7% of my portfolio into Mastercard. It now makes up, along with Amazon and Google, one of my three largest positions. And here are four of the reasons why I invested.

I believe that while most investors view Mastercard as a toll booth, my view of the company as a security infrastructure is nuanced and fundamentally changes how the company should be viewed.

Lack of movement in the last year and a half due to fears that are grounded in potential fears rather than practical revenue misses.

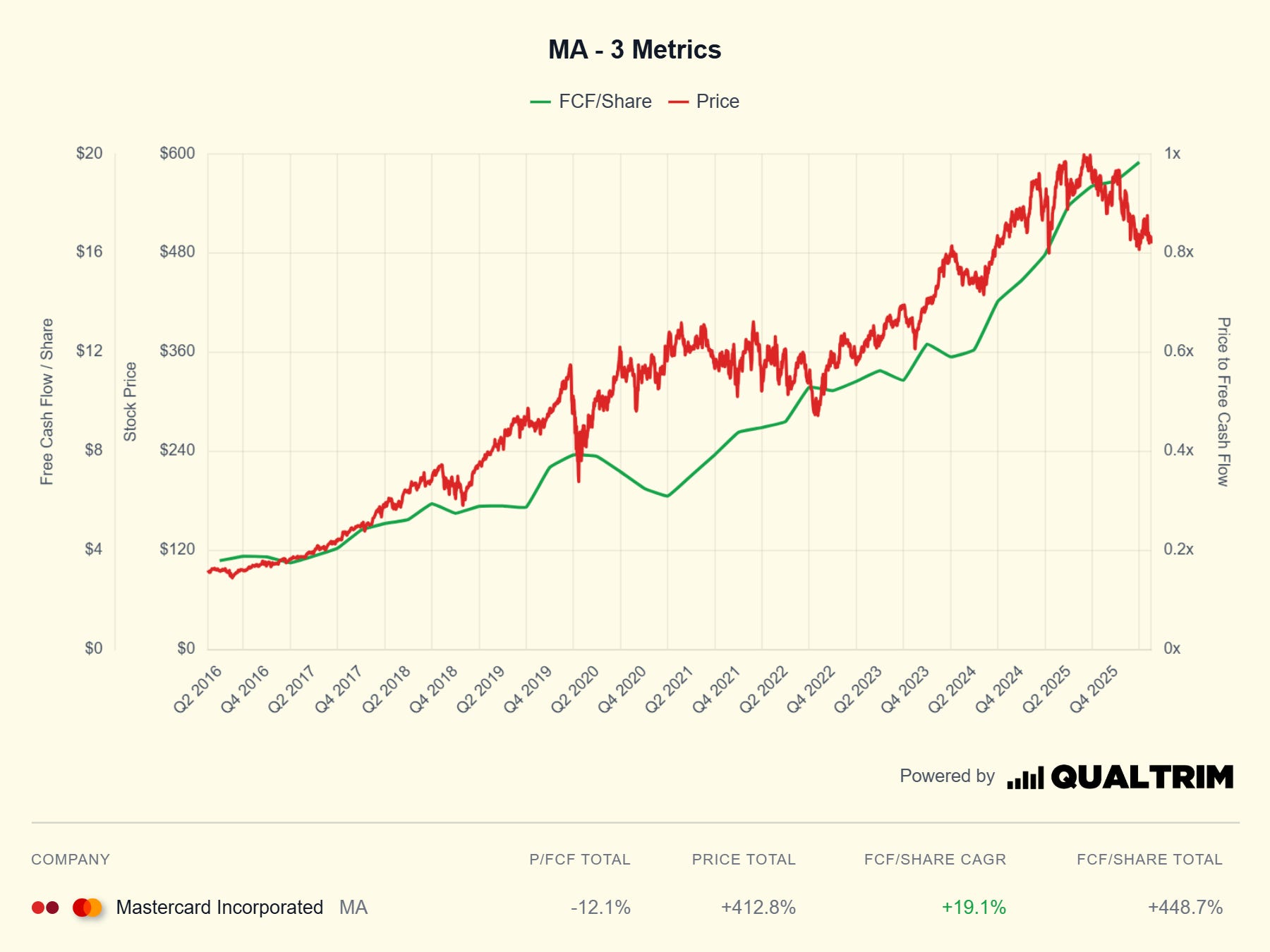

Where the money is, the stock follows. Mastercard has seen a divergence between its free-cash-flow/share and the stock price, something that never stays true for a long time.

Due to their massive buyback program my slice of Mastercard grows constantly larger.

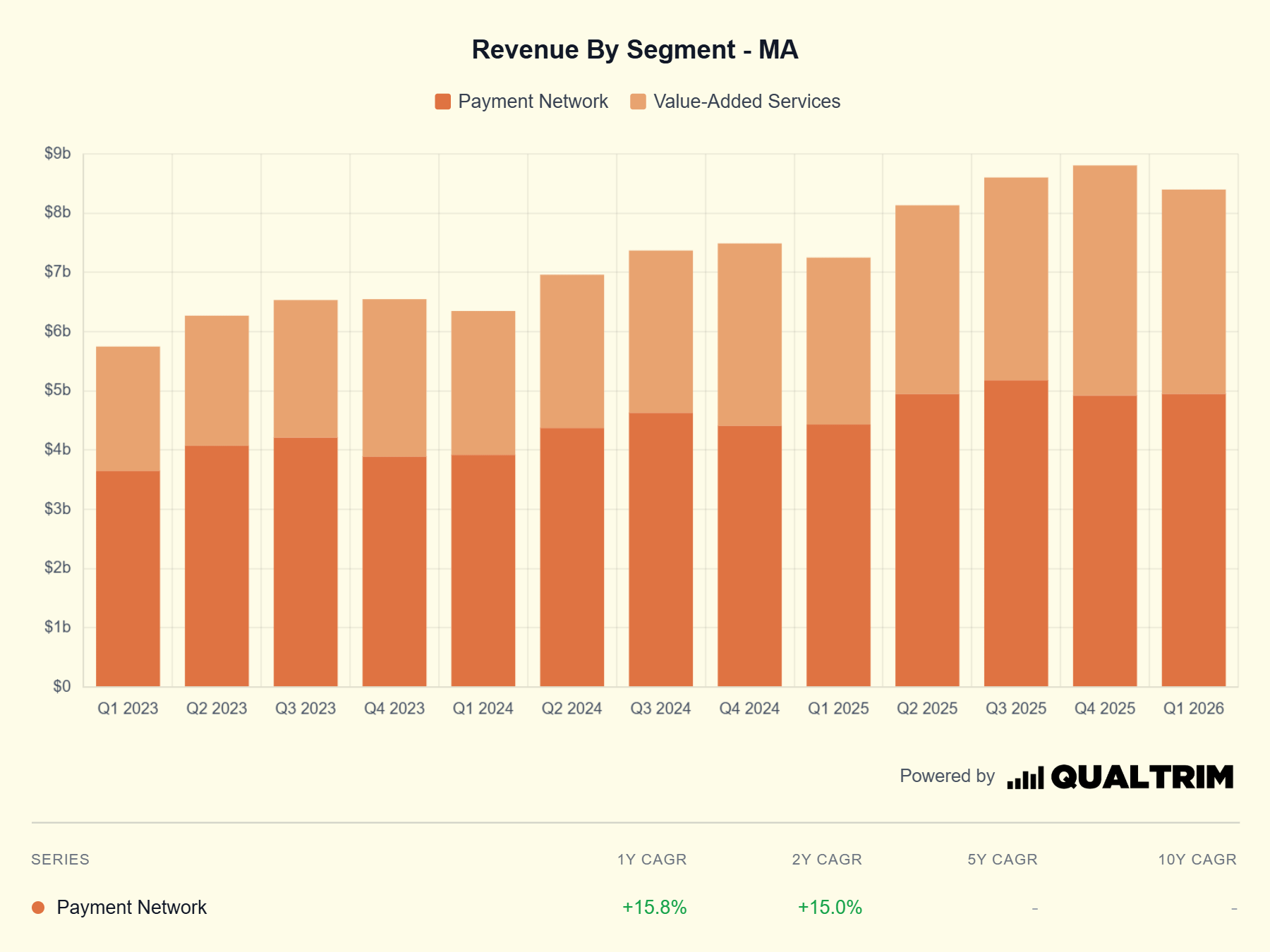

I will start with the typical view of Mastercard. That it is a credit card company that takes fees on every transaction. And while this isn’t wrong, as they made $19.48 billion through their credit card system in 2025, they have another massively underappreciated part of their business; value added services (VAS). These services are essentially things that Mastercard offers that you automatically get when you partner with Mastercard. They include security, fraud prevention, data analytics, and more1. VAS currently represents about 41% of revenue, the highest its ever been.

Security/Fraud Prevention:

Imagine a world that has shifted entirely towards crypto. Everyone has a crypto wallet which makes up their entire bank account. As artificial intelligence gets progressively better, scammers are finding more and more complex ways to use it to prey on those that are vulnerable. We are very close to the point where AI can replicate someone’s voice perfectly. I have been sent AI videos on Youtube, where the sender did not realize that the speaker - Ray Dalio, was actually not the real person but instead an AI version of his voice. While this might be harmless, imagine a world where a hacker calls an eighty year old man, artificially using the voice of his son. The “mans son” (an AI voice that sounds exactly like him), tells him that he needs to send money urgently. The vulnerable eighty year old man immediately sends money, and because it is a crypto wallet, has no ability to get it back.

A payment that goes through instantly is not beneficial to the customer, something I go over in depth in my Mastercard breakdown, which also covers additional thoughts on the company.

Rather than stay away from crypto, Mastercard sees massive potential expansion into that space as well. As the current leader in trust and security they are moving aggressively to establish their dominance there as well23. They have created easy to use usernames, where instead of a long crypto wallet, users are able rename their contact and send money directly to them. This can avoid the situation given above. If the elderly man doesn’t see his son’s name in the crypto wallet, he will know it is likely fraud. In addition, as their data base grows, they can block users who’s accounts seem suspicious and likely to commit fraud. Mastercard is essentially taking their business model that made them leaders in security and pivoting into the crypto world.

Mastercard is also training their own AI model to detect fraud calls. By training their model using millions of scam calls, Mastercard is positioning themselves as a security system that can detect scam calls. Mastercard’s goal is using AI to send an alert in real time to their customers4.

In an age where the ability for fraud is constantly expanding, Mastercard and Visa will be positioned to support crypto safely and provide security, fraud detection and trust layers. This is one of the reasons Mastercard has performed several major acquisitions of different crypto companies, including a $1.8 billion acquisition of BVNK5.

As fraud becomes more sophisticated, trust is more valuable. Mastercard is one of the world leaders in trust and will benefit long term from it.

The next big fear is regulation. Governments are beginning to see Mastercard as a threat to their citizens. This has caused potential regulation, both in the US through the CCCA act and abroad in Europe. The CCCA act however, might try and achieve the right goal, protecting customers, but it gets there using the wrong means, something that Alan Kaplinsky goes in depth in his video with Marisa Calderon about the potential CCCA act6.

“Right Problem, Wrong Solution.” Marisa Calderon

They explain that some of the proposed laws that are supposed to benefit the consumer, will inevitably hurt those same people instead. She explains how a 10% cap on credit cards will cause standards to go up in regulated credit card companies (like Mastercard) and cause them to decline potential consumers. Those potential consumers will then turn to less regulated, more predatory and higher interest loan options.

“Consumers pay the cost… they pay the costs through access laws and through other kinds of product changes that impede their abilities to engage responsibly in the credit markets.” - Marisa Calderon

And there is historic precedent for a government thinking that enacting a major change in credit card law will fix the economy. In 1980, the US was under a period of extreme inflation. To try and fix this, President Carter implemented a cap on credit card companies that ended up being so economically damaging that it was withdrawn after only a few months7. Contrary to expectations, this measure was detrimental. Along with other factors, in just over a month, unemployment rose from 6.2% to 7.8%. Rather than helping, the credit card changes actually caused an additional damage to an already broken US economy. “The controls had a powerful psychological effect. They restrained borrowing, drove down interest rates and slowed down economic activity.8” It was so bad, that US citizens began cutting up their credit cards and sending them by mail to the white house.

And it is for this main reason that I believe the main fears of Mastercard are disconnected to the reality. People often look at a crypto as a huge risk to Mastercard, but I believe customers will often prefer to either stay with Mastercard or use Mastercard’s security system to help protect their crypto wallets. I also believe that governments will realize that often, the best way to protect their citizens, is to allow trusted credit card companies to flourish.

Valuation:

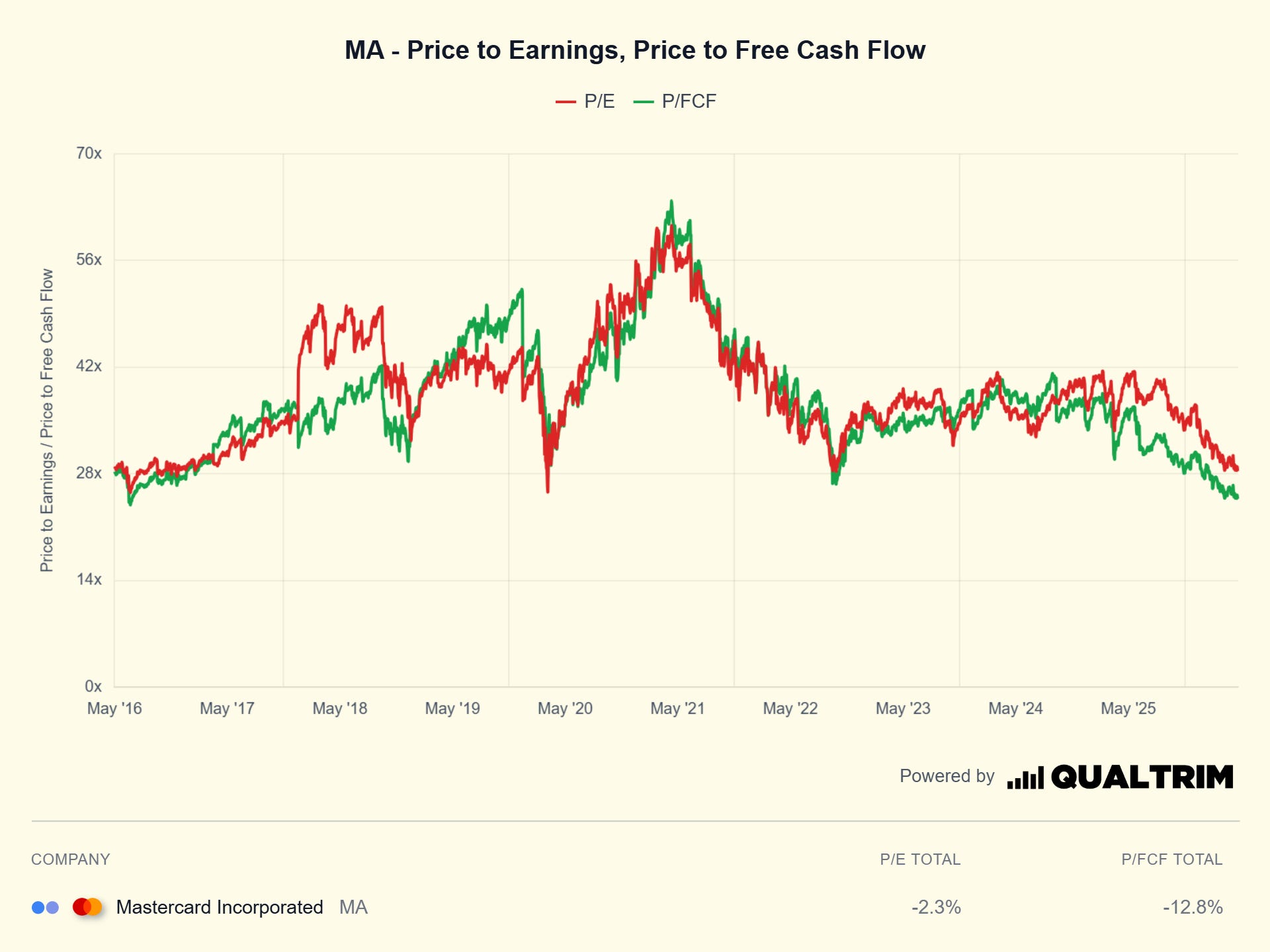

Mastercard’s stock price and free-cash-flow/share are almost always closely linked, as seen by the graph below. Historically, Mastercard’s stock has reconverged with its free cash flow which is why I believe that now is a good time to build up a major position. Simply put, in the graph below, when the stock price is above the free cash flow per share, the stock is expensive. When the lines converge, it is trading at its fair value. When the stock price goes below the free cash flow per share, as seen now, it is a buying opportunity. As seen below, in the last ten years, not counting market sell offs (in which the stock still quickly rebounded in 2020 and 2022), only briefly in the period between 2016-2017 was the stock price below the FCF/Share. In the eight years that followed, Mastercard returned 411%, almost doubling the returns of the S&P .

It is for that reason, that despite Mastercard being up 35% in the last five years, it is actually at the cheapest valuation in the past five years. Both revenue and net income have nearly doubled.

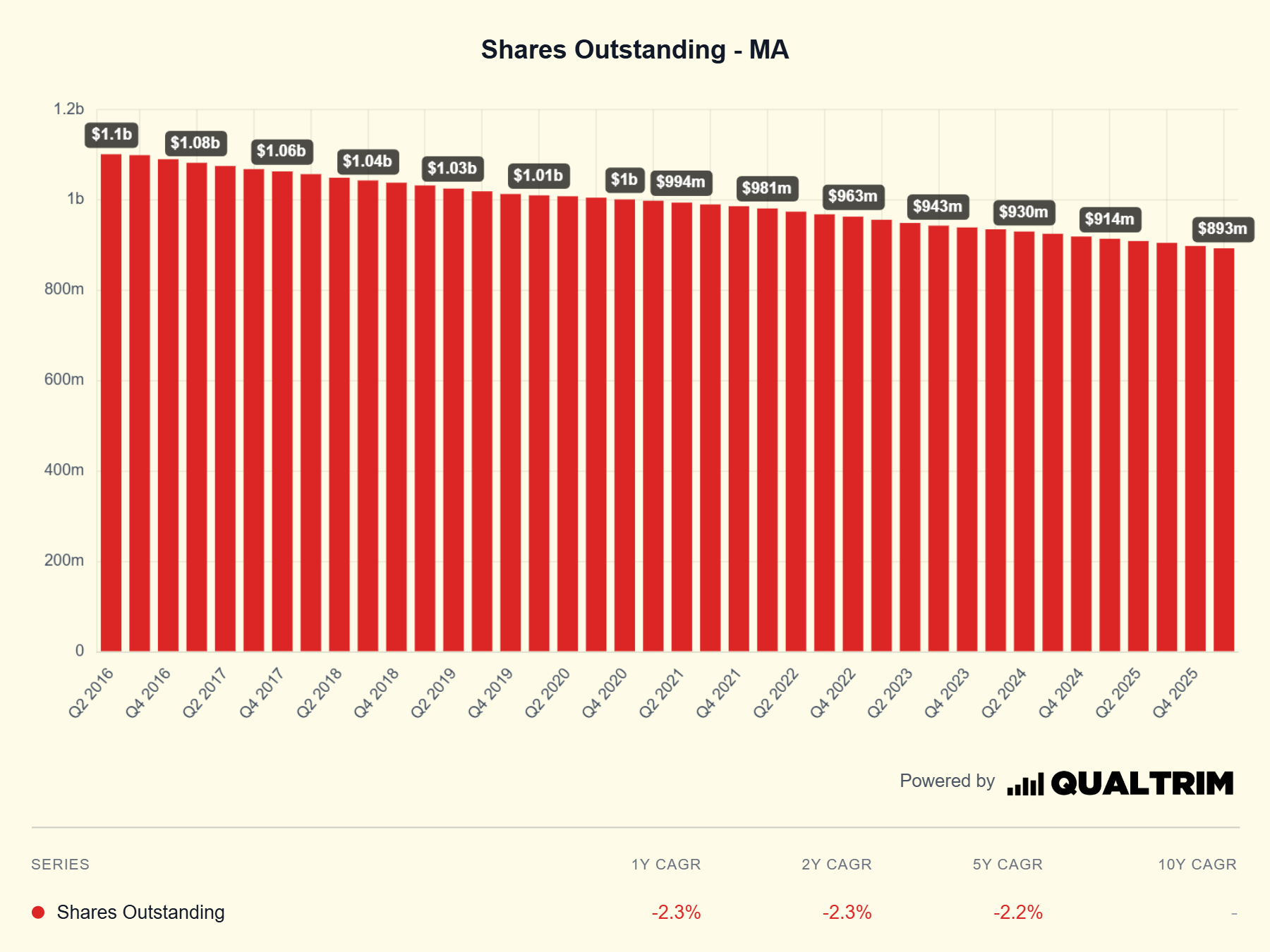

The last factor that makes me very happy to own Mastercard, is their extremely consistent buyback program. In the last ten years Mastercard has reduced their shares outstanding from 1.1 billion to 893 million, a reduction in over 200 million shares. Slightly less than 20% of the company has been retired in the last decade. As the company continues buying back shares, each year of buybacks becomes more and more effective. For anyone who has bought Mastercard shares ten years ago, they now own 20% more of the business than they did previously. Mastercard’s profits are therefore split into significantly fewer slices of the pie. This is a similar playbook to one that Apple employed in order to become one of the largest companies in the world. Looking forward, in 2026, Mastercard announced that they will be repurchasing $14 billion in shares.

Essentially, any dollar spent buying Mastercard today will own a larger percent of the business in a few years. Mastercard’s dividend while relatively small is also growing rapidly. While still relatively small at 0.71%, in the past decade they have consistently increased their dividend by 16% CAGR. As they continue to grow their dividend payout, my share count will continue increasing as I reinvest dividends back into the stock.

DCF Calculator:

While I believe that Mastercard’s fundamentals are excellent it is always important to make sure that you are not massively overpaying for the right business. Mastercard is trading at historically low price to earnings and price to free cash flow. The only times in the last ten years that the ratios were comparable were the 2020 and 2022 market sell offs and a brief dip in 2016.

Still, even though you are getting in at a good price in comparison to historical valuations, it is always important to check that the stock you are buying has long term growth potential. In the past ten years, Mastercard has returned an average of 14.6%. Going forward, I assumed that they will continue growing at 14%, in line with analyst estimates and historical trends and I assumed that the FCF yield will be 3.5%. This is slightly higher than their historical average and leaving significant room for higher upside. As recently as 2021, Mastercard has traded at a FCF yield below 2% and for the most part hovers around 2-3%. If market sentiment improves as fears around crypto and government regulation lessen, Mastercard could vastly outperform the general market. If FCF yield drops 2.5%, this stock could be returning north of 20% per year.

The Fear:

While I believe that Mastercard is incredibly well positioned for the future, the government regulation fear is legitimate. US, European relationships are becoming increasingly strained and hostile. One of the main places where the EU fears being fully reliant on the US is through their payment systems. Due to this fear, European legislators are trying to push forward EU alternative payment systems. While it is extremely difficult to move fully away from US payment giants due to their strength and dominance, European lawmakers can introduce laws that give their own credit card companies advantages over American players. Europe’s Wero, the main competitor already has 43 million users. In addition, this feeling of the need to move away from American companies was strengthened after Mastercard and Visa shut down Russian payments after Russia’s invasion of Ukraine in 2022.

“Visa, Mastercard… Trump can cut everything off. The rest is poetry. I urgently request that the commission organize a European Airbus for payment systems: you can’t say you weren’t warned.” Aurore Lalucq

Even with these legitimate fears, when a historically great stock is trading at a major discount in relation to its historical averages, it is often worth buying. When it comes to Mastercard, I believe that in a time when the stock market is focused fully on AI, Mastercard will quietly continue to compound. It is for that reason that I have made it one of my largest positions.

Disclaimer: For those of you reading this, remember I’m sharing my personal journey and opinions, not professional investment picks. My predictions are based on assumptions that could be wrong, please do your own research before investing.

https://www.finextra.com/blogposting/30482/deep-dive-mastercards-value-added-services-and-solutions

https://www.stocktitan.net/sec-filings/MA/10-q-mastercard-inc-quarterly-earnings-report-0db7b6eecfe5.html#:~:text=BVNK%20acquisition%20consideration%20%241.5B,Key%20Terms

https://www.mastercard.com/global/en/news-and-trends/stories/2025/mastercard-crypto-credential-polygon-labs-mercuryo.html#:~:text=Here’s%20how.,will%20go%20where%20they%20should.

https://www.wired.com/sponsored/story/mastercard-ai-to-stop-scams/

https://gfmag.com/technology/mastercard-betting-big-bvnk-stablecoin/

It’s important to note that Marisa Calderon is the head of a non profit which helps try and advance economic mobility among those facing economic barriers.

https://harvardlawreview.org/print/vol-138/the-federal-reserves-forgotten-credit-mandate/

https://www.nytimes.com/1982/07/17/opinion/keep-credit-controls-on-the-shelf.html

Matercard is great, but im more bullish on stripe for the future