The Case for Mastercard

Why efficiency is not always #1.

Mastercard is misunderstood. They are seen as a payment giant whose value is in earning revenue through fees charged on every single transaction. The common belief is that due to Mastercard’s size they make tens of billions of dollars a year through these fees and this is the core of their business. The people who are bearish about the company, point to other options, National Payment Systems (NPS) or crypto in order to point out the flaw in Mastercard. If I can instantly pay with stablecoin and bypass any fees, wouldn’t that be preferable? Isn’t it better to not pay fees and have a more efficient payment system? And while this is not totally incorrect, this is missing a key aspect to the payment giant. Trust. Mastercard is no longer a company that is just a payment mechanism.

Mastercard or Visa:

Before diving into the analysis, I want to discuss Mastercard’s biggest competitor, Visa. Practically, these are both relatively similar companies with similar products, services and even market caps. Currently, Visa is slightly larger with more transaction volume while Mastercard is growing quicker and puts more of an emphasis on their Value-Added Services (VAS). Visa also has more of an emphasis on the US market and has a more dominant position there while Mastercard has a massive worldwide market. They both give out a similar dividend, with Visa’s being very slightly higher and both are aggressively buying back shares. Overall both are very similar companies and the vast majority of what I write about Mastercard will be applicable as well to Visa. Overall, I chose Mastercard because of their focus on VAS which looking forward will become more and more valuable. And because, well, I use Mastercard.

The Bear Case:

There are a few reasons why despite very strong financial numbers the stock is down 8% in the last year despite the general market being up by 16%.

Trump has proposed (on truth social) a 10% cap on interest rates. My opinion is that these rates likely will not take place due to how much of a negative effect it would have on the economy. One of the most vocal critics, JP Morgan’s chief executive Jamie Dimon said that it would be “an economic disaster…The people crying the most won’t be the credit card companies, it will be the restaurants, the retailers, the travel companies, the schools, the municipalities because people will miss their water payments.” Since floating out the idea over a month ago, it has mostly faded into background noise and during Trump’s recent near two hour State of the Union, it was not even mentioned. This seems like an idea that will not materialize as it most affects the people it is trying to protect, forcing people into riskier and less stable credit methods. In addition, even if the change is implemented it will mostly hit the banks who will then turn to Mastercard and its VAS in order to look for new ways to monetize their data.

Next, many governments are trying to move towards government payment systems that are able to move money quickly. While these payments seem ideal, the main issue is that these payment systems are much less safe than Mastercard. The insurance is nowhere close to what Mastercard offers and this often leads to massive fraud cases. In Brazil, they released Pix, one of the biggest government run payment networks in the world which along with massive use has “simultaneously created a $2.7 billion fraud ecosystem that represents one of the most successful criminal revenue streams in global cybercrime….it is simultaneously the world’s most advanced digital payments market and one of its most dangerous fraud battlegrounds.” The fraud is so prevalent that 2.5% of Brazil’s GDP was estimated in losses in 2024. Nearly one in four Brazilians are affected by cybercrime in a twelve month period and only 9% get their defrauded money back1. Here, where theft is so prevalent, Mastercard can offer an incredible valuable service: safety. They offer massive cybersecurity and data in order to make these services safer.

“Visa, Mastercard… Trump can cut everything off. The rest is poetry. I urgently request that the commission organize a European Airbus for payment systems: you can’t say you weren’t warned.” - Aurore Lalucq

This isn’t exactly to say that Mastercard is impregnable. Europe specifically seems to want to move away from US products due to a growing divide between Europe and America, largely because of Trump and fears that the US no longer treats them as the ally it once was. Europe has begun to push out Wero, a European digital wallet that has already scaled to over 43 million users and is aimed at reducing Europe’s reliance on Visa or Mastercard. These services have been pushed by people like Aurore Lalucq, Chair of the European Parliament’s Economic and Monetary Affairs Committee who has been extremely vocal about moving away from US financial companies saying “Visa, Mastercard… Trump can cut everything off. The rest is poetry. I urgently request that the commission organize a European Airbus for payment systems: you can’t say you weren’t warned.” This came after Visa and Mastercard suspended payment in Russia after the invasion of Ukraine in 2022. Again Mastercard’s shift towards VAS is once again instrumental here as they position themselves as a security infrastructure and service layer that can be used in addition to any payment mechanism, rather than just a credit card used to pay. In addition, Mastercard has begun integrating stablecoins and today their network is now tokenized - allowing you to use crypto at over 150 million merchants. Mastercard is trying to become the safe bridge needed in order to use these new payment systems. Still, these are legitimate concerns and only time will tell how Mastercard will fare.

The Value of Using Someone Else’s Money:

The number one most important thing for customers is efficiency right? That’s what most people would think. Most people would say that a “middle man” is inherently a net negative and by cutting him out you would have a more efficient product. This argument argues that the ideal payment is one done in seconds, where the money goes from the customer to the merchant instantly. I buy tickets to a concert using stablecoin and within seconds, the money is now in the domain of the merchant. But if you consider it for a second, there is something much more important to a customer than efficiency, safety. When the money is instantly deposited into the merchant’s pocket, I have no ability to get my money back unless the merchant graciously decides to refund me. On the other hand, if I buy a product using a credit card, I have a safety net. If the product is a scam, or if my card is stolen, I can cancel the payment and get my money back. When the customer uses a credit card, Mastercard has a strong incentive to resolve fraud because the money being spent is the bank’s capital not the consumers cash. In addition, not only will they return my money to me, they will flag that product as suspicious, and if enough data is accumulated proving the merchant or product to be a fraud, Mastercard will no longer authorize the payment and save the customer and itself from potential fraud cases.

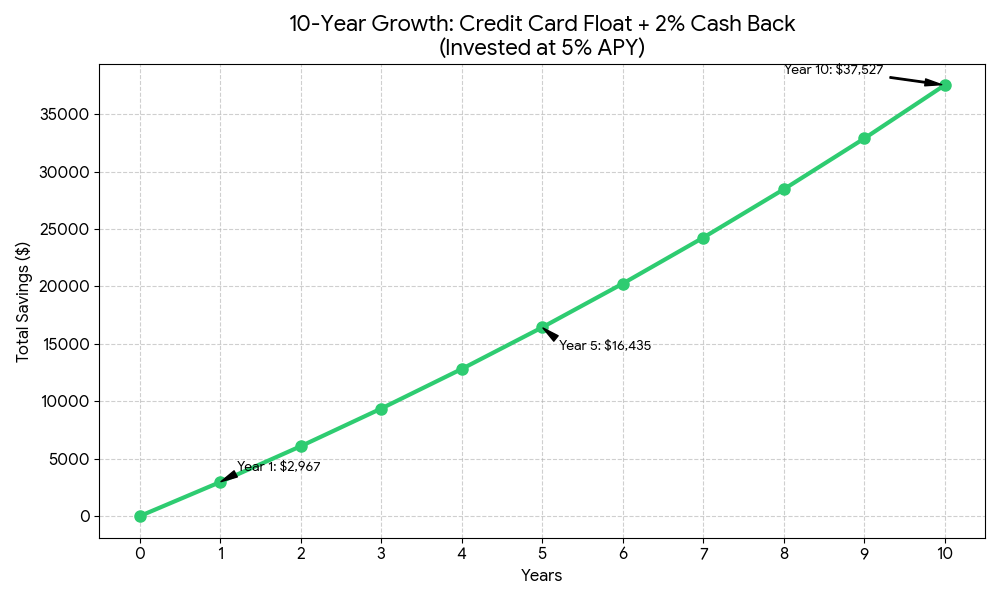

Another benefit of using Credit Cards is cashback - many cards offer 2% cashback on every purchase using the card, which can add up to significant amounts over time. Finally, another often overlooked benefit with using money that is not your own is that you don’t actually pay the money until your payment cycle days later. Therefore, you are getting a “free loan” from your credit card company. This “grace period” lasts anywhere between 21-55 days depending on when exactly you buy the product. While this may not sound like a huge deal, if you have a monthly payment, the difference between paying at the beginning of the month and the end can be notable.

Imagine that you have a monthly payment of $10,000.

Option A: You use a debit card that instantly leaves your account on the first of the month every year. You spend $120,000 in one year and get $0 invested at 5% per year.

Option B: You use a credit card and leverage the bank’s money as a $10,000 “float” while investing your own money and having it work for you. In the first month, your money invested at 5% a year is earning $41.67 a month. The money increases slightly and by the end of ten years you will have $6,475 from interest AND an additional $31052 from the 2% cash back. Significant money saved.

In addition to the added benefit to the customers, this VAS is also beneficial to the merchant, who is also afraid of being scammed by a customer who will dispute the transaction immediately after it happens. The merchants are willing to pay a small premium in exchange for guarantees that they will deal with customers who will pay, or at least Mastercard will. This is one of the reasons why the VAS section is growing so fast, it is an agreement that is beneficial to both the merchant and the client.

Value Added Services:

The next part of Mastercard that makes it an extremely valuable and fast growing company is their Value-Added Services. These are different services that are not connected to the payment fees themselves and include many different services.

Cyber and Intelligence (Fraud Prevention, Identity Solutions and Cybersecurity to name a few) and Data and Services (Insights and Analytics, Personalization, Consulting), are two of the main leading ones. While we touched on the fraud prevention in the above section, the data they own can also be incredibly powerful. For a company like Starbucks who wants to know where the best place to open a new branch is, they can go to Mastercard and using the billions of transactions across millions of customers identify spending clusters. Using that information they can find out exactly where the most profitable place to open a store is. Mastercard will take a fee in exchange for the information they provide that these companies would not be able to have without them.

While the revenue of the payment network “only” grew at a 14.5% growth rate in the last five years - and 12% in the last year, their VAS have grown at an incredible 19.8% per year in the last five years - and 23% in the last year. In 2015, VAS made up only 18% of their total revenue. Last year in 2025, that percent jumped to 41%. VAS has now become the main driver of the stocks P/E multiple. This transforms Mastercard from a pure credit card company to a cybersecurity meaning the multiples could potentially jump even higher. These services are also less likely to be targeted by the government, who see fees as targeting while VAS they see as security.

Financials, Buybacks and a DCF calculator.

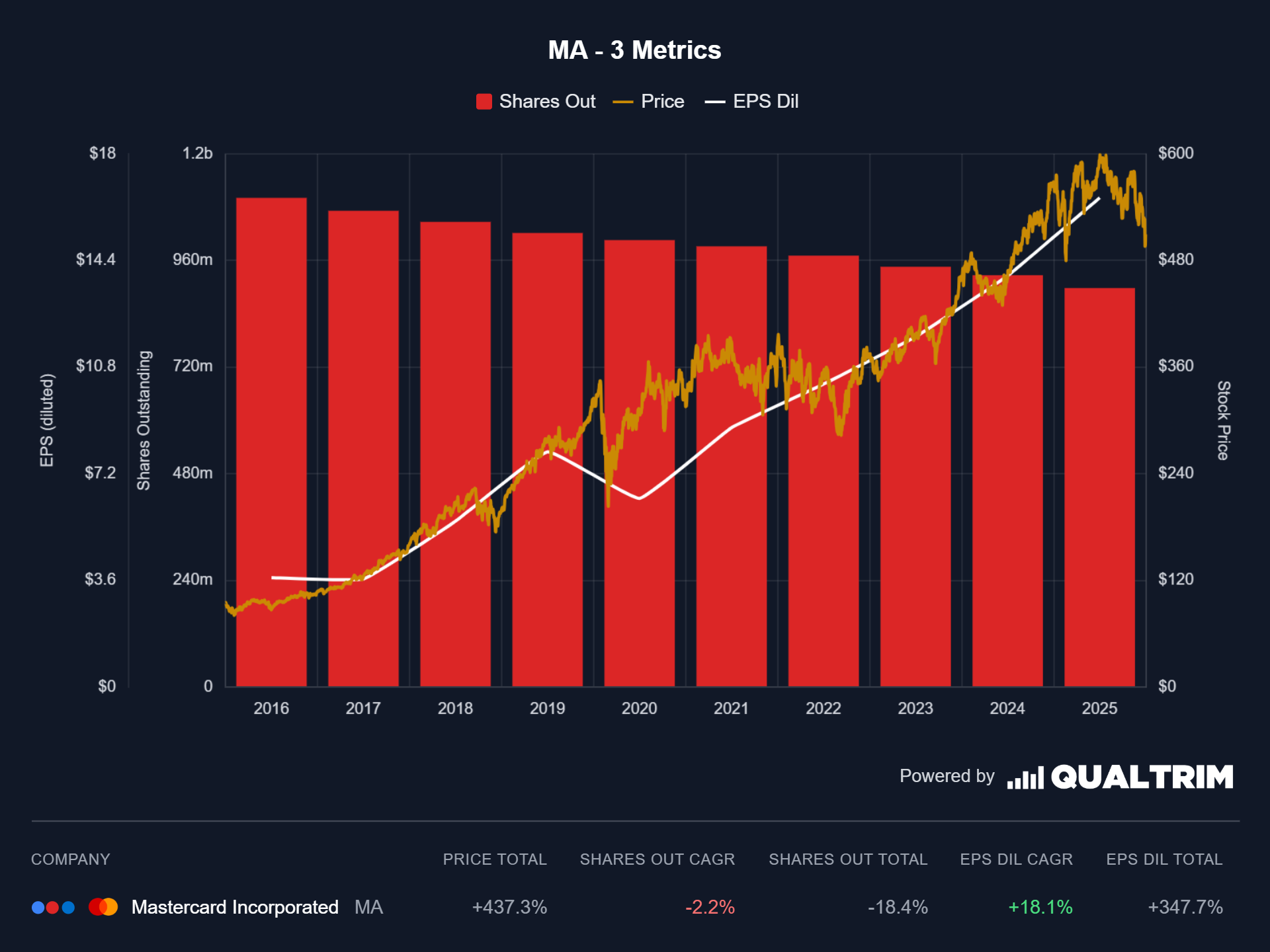

Mastercard clearly believes in a strong buyback strategy which is why over the last ten years the company has purchased back over 300 million shares, at a rate of 2.2% per year. In the last five years, this buyback strategy has sped up to 2.5% per year. This year, the board agreed to $14 billion worth in buybacks so we can assume they will continue aggressively buying back their shares going forward. To the naked eye, this may not seem so significant but if Mastercard continues at this pace by 2030, EPS would be projected to double assuming they continue increasing revenue by 15% annually. An EPS increase of this size likely means that the stock price will increase due to the company being more efficient at making money for you. In the chart below you can see that as the shares of the company go down, the EPS increases and the stock price follows extremely closely. This aggressive buyback strategy has been similarly used by Apple over the last decade to grow the company more than tenfold in the last decade.

Next, if we use a DCF calculator to understand what the stock price will look like in the next five years we see extremely positive signs. I assumed that the EPS growth rate would be 16%, slightly slowing down from the 18% they have returned in the last ten years. I used a PE Multiple of 30, which is what it currently trades at, a number 15-20% lower than its ten year average. Using these numbers, I get a 15% average return from today’s price and a current entry point of $646 if I want 10% returns. According to this calculation, the stock will nearly double in the next five years.

While there are legitimate concerns around Mastercard, I believe it is positioned incredibly well looking forward as they continue buying back shares and increasing their revenue from their Value-Added Services. These services, beneficial to both client and merchant will only continue to grow in the coming years. Mastercard and Visa are such massive duopolies that in my opinion it is hard to imagine the stocks tanking long term and therefore these companies have upside and relatively capped downside making this an asymmetric bet. Mastercard continues moving to a multi-faceted company offering multiple different valuable services and I believe going forward they are poised to continue offering market-beating returns as their value is further realized.

Disclaimer: For those of you reading this, remember I’m sharing my personal journey and opinions, not professional investment picks.

All the stats here are from an in depth article about called “The PIX Paradox”. https://www.scamwatchhq.com/the-pix-paradox-how-brazils-payment-innovation-became-a-2-7-billion-fraud-magnet/

The trust piece is the one that often gets glossed over when people talk about faster payment rails. Faster doesn't always mean safer, and when money moves instantly, it also moves irreversibly. That trade-off matters differently depending on whether you're buying coffee or paying a supplier.