The Case for Uber

Breaking Down the Next Chapter in Uber's History.

Uber: Not Just a Taxi Service, an Infrastructure Layer.

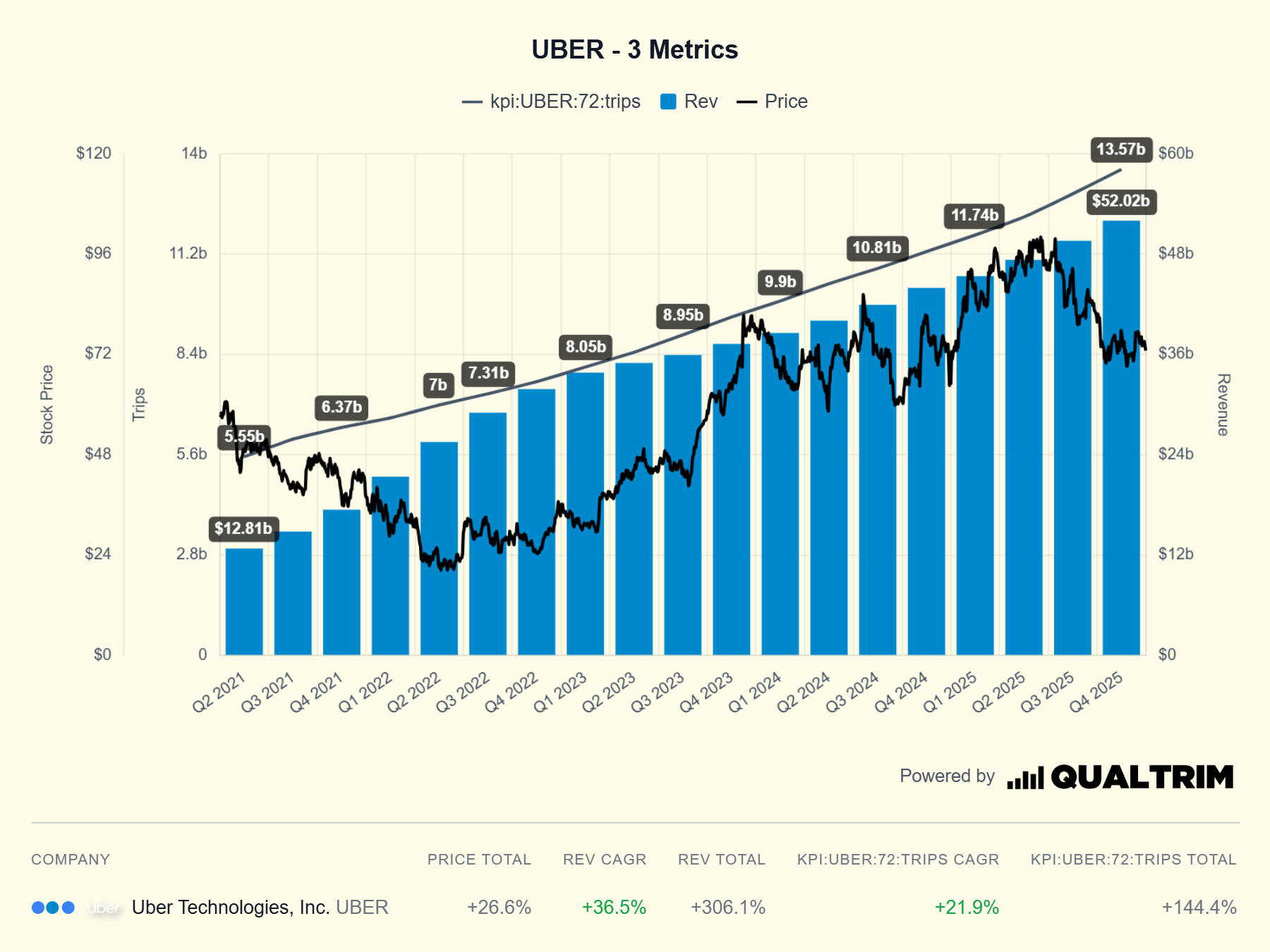

Uber has increased revenue by over 400% and has more than doubled the amount of trips taken in the last five years. They have turned Uber from a struggling business burning cash, into a profit machine, yet stock still trades like a business under existential threat. Uber’s stock is repeatedly dislocated from its financial metrics as it often seems to trade on hype and story lines, both positive and negative. This is a stock that is priced for disruption, specifically from mounting competition and autonomous vehicles (AVs). In this breakdown, we will look at why Uber is down in 2026 and whether the stock is a buy today.

The Business History:

Not so long ago, in order to order a taxi, you needed to either flag one down or call a taxi hotline, where you told the dispatcher your current location and where you wanted to go. A few minutes later, a taxi was supposed to show up. It didn’t always, which was why sometimes you needed to call back and request a second taxi to pick you up.

In 2008, Taxi Magic (today known as Curb) changed the game. They allowed users to order, track and pay for rides from the comfort of your smart phone. The only catch, they didn’t own their cars. Instead, they integrated into the taxi system of the city they were in.

Then, a year later in 2009, Uber was founded. Originally, they were founded as a high-end black car service that you could order, track and pay for directly from your phone. The difference, Uber didn’t own its vehicles, instead, it hired drivers to drive using their privately owned cars, a system that still runs until today. Within a year, Uber began testing in San Francisco and on July 5th of 2010, they officially drove their first trip1. By 2012, they had officially launched UberX and had become mainstream in cities all across America and Europe.

Today, Uber splits up their revenue into two categories, mobility and delivery. Mobility is getting people from point A to point B, delivery focuses on food and groceries but also includes an ability to transport packages, documents and even gifts.

To understand Uber, you have to stop looking at it as a “ride-sharing company.” In 2026, Uber is a multimodal logistics platform that owns the relationship with the consumer for almost every physical movement they make. Whether it’s a person, a pizza, weekend groceries, a pallet of freight, or a pair of sneakers, if it moves from Point A to Point B, Uber is building the digital rails for it.

The Business Today:

Uber now has 10 million active drivers and roughly 1-1.2 million active drivers on the road in the US at any time2. Over two hundred million people use the app monthly either for food delivery or rides across 70 countries and 15,000 cities worldwide. In the US, Uber dominates the ride sharing market with 76% of rides being ordered on their platform.

Uber has also rolled out a yearly subscription service called Uber One that gives members special benefits like $0 delivery fee and credits back for every purchase. Despite being only rolled out in December of 2021, less than five years ago, Uber One has been incredibly successful so far with currently over 50 million users. Uber One customers also spend significantly more, on average spending 3.4x as much as non-members3.

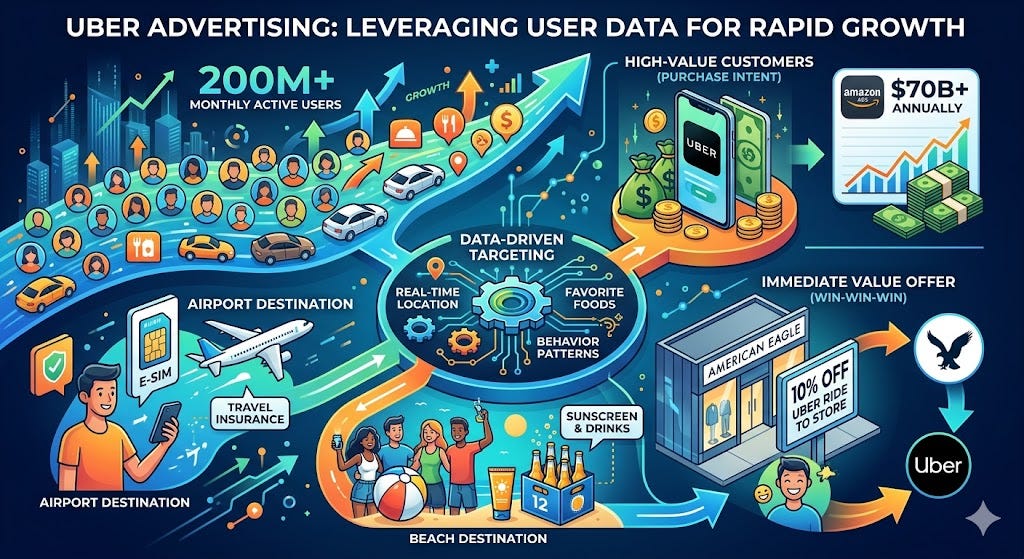

By leveraging their 200+ million monthly active users, Uber has been able to grow its advertising business rapidly to over a billion dollars in 2025. Uber users are inherently high value customers as anyone who opens the Uber app has an expectation that they will be spending money. This is similar to Amazon, which has now grown its advertising to almost $70 billion yearly. Even more valuable to advertisers, Uber knows exactly where their users are traveling to and from, what food they like and when. Uber can therefore target based on location, giving someone traveling to the airport an advertisement for an E-Sim. Uber has also shown that ads that offer immediate value make users more receptive. For example, American Eagle can offer 10% off an Uber ride to their store, providing a win-win-win for Uber, the consumer and the advertiser. Lastly, Uber has also introduced screens into many of their cars. While still at the beginning of rollout, the 75,000+ screens show JourneyTV which provides users with in-ride entertainment and advertisements. “The average user ride is now 20 minutes… We are starting to think more and more about what could that personalized experience be.4” Uber wants to monetize ride time while also improving the user experience.

Overall, advertising is a healthy, growing business that will continue to expand as Uber continues growing and learns more data from its customers.

There are also legitimate concerns with the business. Lyft and other competitors have proved serious competition and the future move towards AV is something that scares many investors off. Furthermore, there is a push among some legislators to have Uber treat their workers as employees, rather than independent contractors, which would give Uber drivers additional benefits that would compress margins. These are all complex problems that Uber will have to properly navigate going forward.

The Business Positives:

Uber hasn’t always been profitable. As recently as 2022, they posted a $9 billion loss. However, they have recently been able to turn that around. In both 2024 and 2025 they reported $6.9 and $9.76 billion dollars in free cash flow. What was once a company struggling with profitability, has now become a cash making giant.

Incredibly, Uber is extremely asset light. Uber has only $2.5 billion in physical assets, a number comparable to Visa - $3.0 billion and Mastercard - $2.3 billion. This is due to Uber’s fleet not actually being owned by Uber. Uber, the world’s largest taxi company, owns no cars.

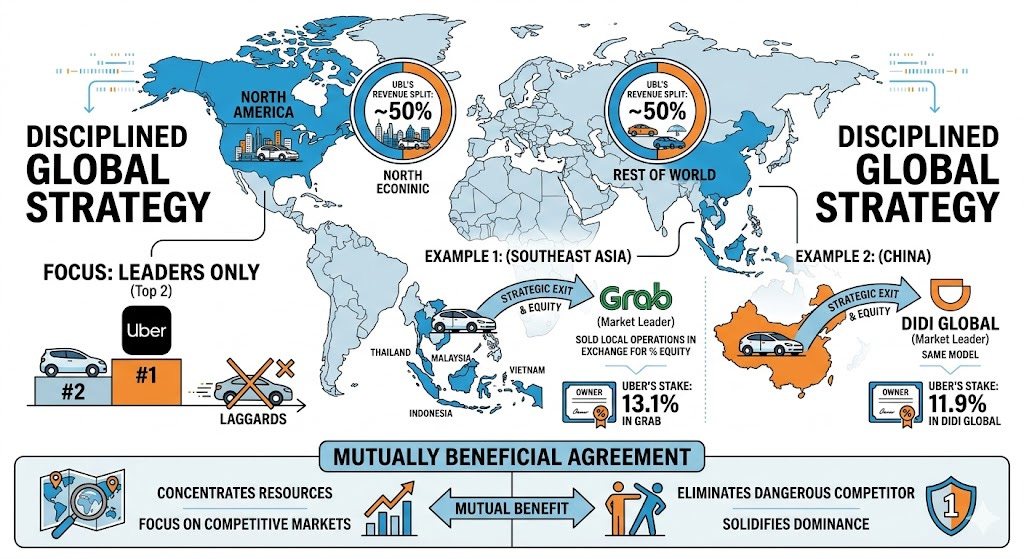

They are also well diversified globally. Their revenue is split evenly with around half being in North America and the other half being outside of it. More than that, management shows high levels of discipline by focusing only on countries where they are the first or second option. In countries that they aren’t leading, they will usually sell their local operations in exchange for a percent of the leaders. In South East Asia, instead of competing with Grab and Bolt, the dominant ride sharing platforms in those regions, they sold their stake to Grab and in exchange acquired 13.1% of the company5. In China they did the same with Didi Global in which they own 11.9%. This is a mutually beneficial agreement, Uber owns major stakes in companies that become more dominant in the region and the companies trade part of their ownership to get rid of a potential dangerous competitor. It also allows Uber to focus its resources and time in markets that they are already competitive or dominating.

And due to this focus it has become so dominant that it has even managed to enter the English language. Uber has managed to become a “proprietary eponym” - a brand name that has grown so large that it is now used as a generic term joining the ranks of giants such as Google, Kleenex and Band-Aid. Even more impressively, “Call your Uber” is now used in slang to tell someone they are being annoying and should get lost6.

Management is also seen as a big positive for those investing in Uber. The current management, led by Dara Khosrowshahi, has been credited with turning Uber into a profitable company. Their decisions to exit underperforming markets has been heralded for making the company more efficient and effective. They also managed to improve their advertising business creating an additional revenue stream that is not connected to their core business. One place where management isn’t popular, is among Uber drivers themselves who often feel like they are being managed by an algorithm with a lack of human support7.

Autonomous Vehicles:

The main bear case with Uber lies with Autonomous Vehicles. The thesis is that Autonomous vehicle companies, like Tesla and Waymo will move into and dominate the ride sharing world. They will cut out the middle man in Uber causing Uber’s margins to compress, brand loyalty to fade and Uber to be phased out.

However, Uber isn’t planning to sit idly while autonomous vehicles race by. Uber has already partnered with a dozen AV companies including massive partnerships with Waymo, Rivian and Lucid Motors. These early investments ensure that Uber will remain integrated and relevant in the AV ecosystem as it develops while also owning parts of these businesses as they grow. There is no indicator that the AV market will be a winner takes all market and these strategic partnerships could be compared to Nvidia owning significant stakes in nearly every AI growth company.

But the bull case is even stronger than their strategic partnerships. While there will likely be dozens of AVs with the capabilities of offering ride services in the next decade, humans will not want a dozen different apps. AV companies that finally have a fleet ready to launch will want to maximize their available vehicles, not fight to gain users on their app. This will likely lead these companies to strategic partnerships with Uber, rather than trying to onboard new customers onto their apps. There aren’t many possible exceptions to this rule.

One possible exception and interestingly a company that hasn’t yet partnered with Uber is Tesla. Tesla has a massive fan base and Elon Musk’s following along with his acquisition of X can spearhead the massive campaign needed to download the Robotaxi app in order to compete with Uber. And Tesla has already begun this campaign to compete with Uber. In its first day on the app store, the Robotaxi app got two million downloads. Robotaxi has also been significantly cheaper than Uber, with users paying less than half the price for the same ride8. The tradeoff has been in wait time, users riding with Tesla have had an estimated wait time of around 15 minutes, compared to three minutes with Uber. As Tesla scales, the question will be can they maintain these lower prices while reducing wait times to something comparable to Uber. Musk has a legitimate chance to pose a long term threat with Tesla, something that Tesla holders feel is one of their strongest points.

Tesla will likely emerge as one of the few competitors with the brand strength and distribution needed to challenge Uber down the line. However, I believe that most AV companies will decide to partner with Uber instead of trying to create their own ecosystem from scratch in a similar way that Toyota partnered with Uber instead of setting up a competing ride sharing app.

Humans at the end of the day are creatures of habit and they will prefer continuing using an app they know and trust rather than downloading dozens of different new AV apps.

There are many reasons why AV companies will prefer to partner with Uber rather than trying to build their own app. Uber has a massive amount of data that will help maximize the efficiency of AV fleets. For example, the amount of users needing ride sharing massively shifts throughout the week9. This would mean that unless a potential AV company produces enough vehicles to cover even peak hours, there will likely be multiple different companies vying for competition. If an AV company does decide to produce enough vehicles to cover even peak hours on a Friday night, they would have 95% of their fleet sitting idly by on a Monday night. Instead, these companies can produce fewer cars and maximize their efficiency by partnering with Uber. Uber will make sure that their vehicles are constantly in use while providing human elasticity to cover for peak hours.

If AVs become the future of ride sharing, Uber’s dozens of strategic partnerships and use of their expansive network will be vital for AV companies to maximize efficiency. AV companies may be able to do the driving, but they need Uber in order to maximize the dispatching and efficiency.

The Valuation:

While I began writing before earnings were released today, post earnings the stock jumped around 9%. Even so, Uber is currently trading at a P/E of 16. It’s price to free cash flow is currently at a 15.4, significantly lower than its 52 week average.

I believe that a few main factors will contribute to multiple expansion for Uber.

AVs will prove to be a boon to their company rather than hurting margins.

Advertising, their highest margin business will continue to rapidly expand.

Uber One will continue to grow causing more customers to turn into loyal, high use customers.

I believe these factors will cause their P/E to move towards the 20-25 range, more in line with the market average. Their EPS will also grow due to earnings growth and continuous buyback program in which they have allocated $20 billion in 2026 to share buybacks. Uber will therefore realistically grow margins and experience multiple expansion leading to a stock price that will likely rise in the next few years.

For my DCF calculator, I used a free cash flow model instead of EPS due to Uber being asset light and still in its growth stage. I assumed an 18% FCF growth rate, at the lower end of Wall Street analyst predictions for Uber. I assumed that their FCF Yield stayed relatively flat at 6% - slightly lower than the 6.5% it is trading at today, meaning that the market will value the business similarly to how it does today. Using these relatively conservative assumptions, Uber will return 18.5% in the next five years. If the market does decide to rerate Uber due to a 9% FCF yield due to Tesla scaling and potential regulatory pressure, assuming it manages to grow FCF by 16% per year, it will still return 7% per year, underperforming the market but still returning solid returns. Under more bullish assumptions - 4.5% FCF Yield and 22% FCF growth rate, the stock could potentially return 30% per year.

Uber has also attracted institutional investors. Bill Ackman, currently holds Uber as his second largest position in his Pershing Square Capital hedge fund. For someone like Ackman, who’s entire portfolio is made up of only eight stocks, a $2.5 billion investment into Uber shows extreme confidence in the stock and its management and reinforces the institutional bull case.

Summary:

Uber seems like an opportunity for a potential asymmetric bets in the market today. The main bear case is something I believe will actually end up helping Uber in the long term. Despite its jump after earnings yesterday, I believe that this stock still has significant room for growth going forward. I think there is a decent chance that Uber crosses their all time high stock price of 100 within the two years and continues growing after that. If not, even if margins compress and growth slows, the DCF model used still returns 7% annually, a high upside for a bear case.

Disclaimer: For those of you reading this, remember I’m sharing my personal journey and opinions, not professional investment picks. My predictions are based on assumptions that could be wrong, please do your own research before investing.

https://matrixbcg.com/blogs/brief-history/uber

https://www.notta.ai/en/blog/uber-statistics

https://www.drewcohenmoney.com/fiveminutemoney/uber-stock-breakdown#

https://www.wallstreetzen.com/stocks/us/nasdaq/grab/ownership#:~:text=Insider-,Name

https://www.huffingtonpost.co.uk/entry/call-your-uber-meaning-meme-tiktok_uk_69e2144ce4b09c81bf175153

https://www.businessthink.unsw.edu.au/articles/uber-algorithmic-management

https://www.pcmag.com/news/tesla-tops-robotaxi-rankings-on-price-but-comes-last-for-convenience

https://quartr.com/insights/edge/where-to-the-story-of-uber

Great breakdown. I like the point that Uber is no longer just a ride-hailing app, but a larger consumer infrastructure platform across mobility, delivery, ads, subscriptions, and eventually autonomous vehicles. The AV partnership angle is especially interesting because it changes the common view that autonomy will only hurt Uber. #On the weekend, I drive some time Uber, so I know the pain.

FYI two class one railroads will be using Uber to transport their workers.