The Case for Meta

Will massive AI spending strengthen a $1.6 trillion empire.

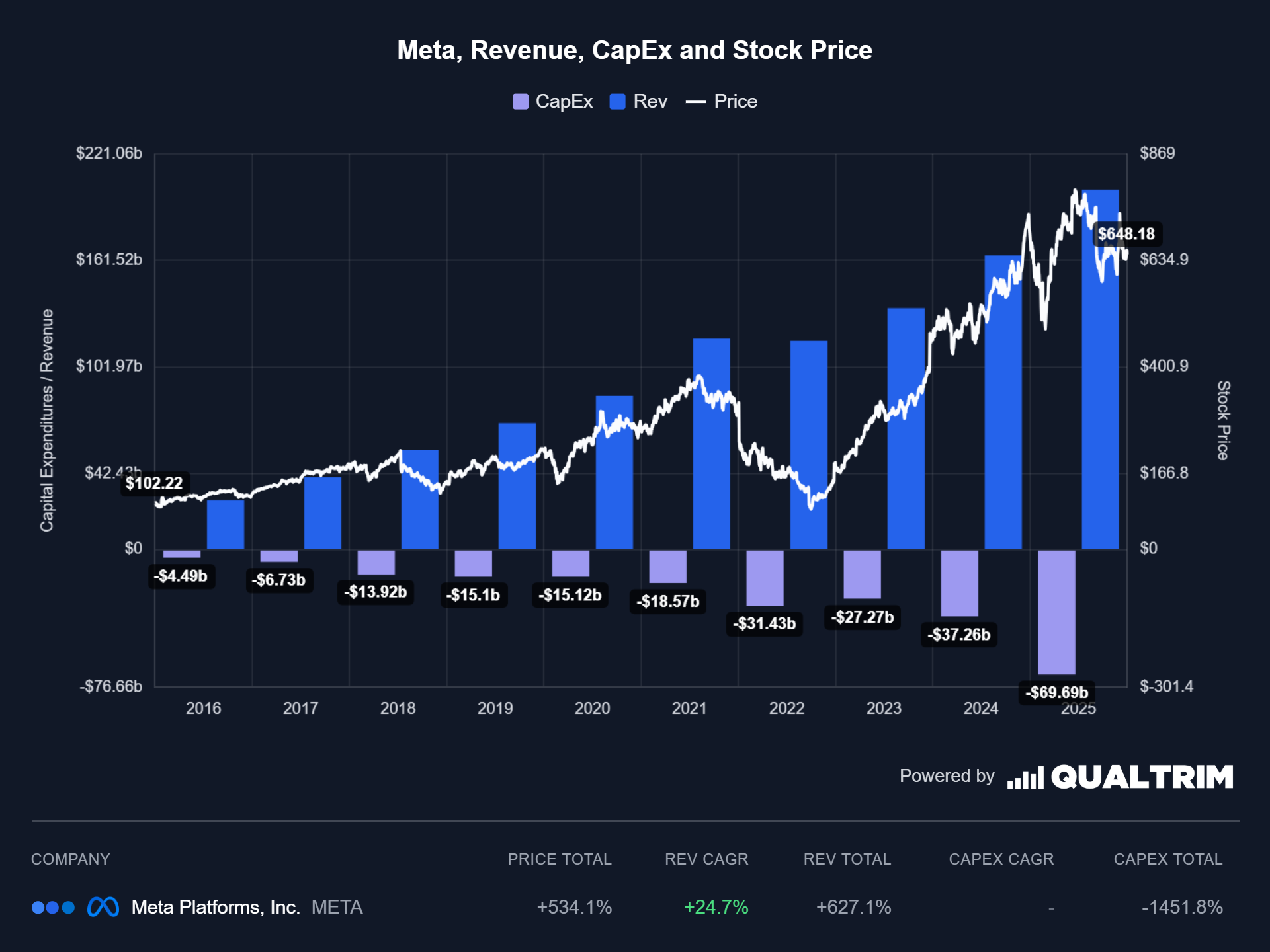

The social media powerhouse just announced that they will be spending between $162-169 billion on total expenses in the upcoming year. This is a staggering number, and to put it into perspective, this is more than the net worth of Target, eBay and Warner Brothers combined. The catalyst, AI spending. Meta, not wanting to be beholden to anyone else, is trying to get ahead of other companies and build up the needed infrastructure early. The question is, will this high stakes bet be profitable or will Meta be digging themselves into another “reality labs” spending hole that ends up tanking the stock price once again.

Meta Platforms:

What was once Facebook and has now expanded to multiple different companies, totaling over 3.5 billion daily active users, is one of the most divisive companies in the world. Valued at over $1.6 trillion dollars, Meta now boasts daily activity from almost half the world’s population through Facebook, WhatsApp, Instagram, Threads and Messenger. Facebook and Instagram represent the classic social media side of the company while WhatsApp and Messenger are Meta’s messaging platforms. Finally, Threads is Meta’s quickly growing competitor to X (formerly Twitter) with 150 million daily active users. As of currently writing this on March 2nd, Threads is #4 on the Appstore, only behind three LLM apps. Overall the Meta Platform is massive and if you’re reading this you most likely are spending significant portions of your time on at least one if not multiple of their apps every day.

The Vision:

Mark Zuckerberg is a controversial figure but even his harshest critics will admit that he is a visionary. For example, one of his dreams ten years ago, which is finally somewhat coming to fruition, was his Reality Labs. These have included all sorts of futuristic products that have been black holes of money, costing $100 billion since the idea was first founded in 2014. Recently however, Meta has pivoted releasing their Meta glasses that are a pair of “AI glasses (that) blend form and function, helping you stay connected and present—in style.” Meta has partnered with Ray Ban to make relatively cheap glasses (now $299) that are both cheap, stylish and multifunctional. Using these glasses you can play music, view notifications, navigate, take photos and videos and dozens of other functions. While the Reality Labs investment has been seen by most as a failure, Meta has pivoted and instead of asking people to leave reality they have tried to enhance it. Meta glasses are viewed as a success, with over 2 million units sold in 2025 after sales more than tripled. Zuckerberg has spoken about how he views these glasses as the future of technology. In an interview with Cleo Abram he says that he believes glasses are “the next major computing platform… the ultimate product… glasses are going to be the ideal form factor. They are positioned on your face to see what you see and hear what you hear.” He talks during the interview about the trend that technology has become more natural and while the first computer was as big as a desk, we have now gotten to the point where a phone fits in our hands. He believes that we will move past phones saying, “it’s pretty unnatural right, it takes you away from the world around you… computing gets more natural…. you want to be able to interact with the world around you, I think this is going to be the next major platform after phones.” Whether or not he is right, he definitely believes that virtual reality is the future and has invested billions into it. If glasses become mainstream, the data available to Meta who would be able to see what you are looking and hear what you are hearing is endless. Will glasses be the future and will his investment finally pay dividends? Only time will tell, if yes, no one is positioned better than Meta. No matter what, the majority of the capital has already been invested and Meta is still an extremely profitable company. I think this is similar to Google’s Waymo, if it works, it will be another huge addition to what is already one of the most valuable companies in the world. If not, they can fall back on their other streams of revenue that continue making the company hugely profitable year after year.

The Ethics:

Meta may be a sound financial investment, but I think when investing in companies there is perhaps another important factor with which to look at them. Meta’s products have caused lots of good in the world. I use WhatsApp daily to speak to my family, who live thousands of miles away. Facebook marketplace is used by a billion people a month to exchange goods. Instagram has created millions of jobs through their platform. Meta has built relationships, fostered friendships, created jobs and facilitated communication for the world at large. But Meta, as the dominant social media in the world has also done other things. Social media has raised rates of depression and anxiety, made people feel worse about their bodies and lives in general and, ironically, increased loneliness and isolation. It has also fostered a world of cyberbullying and online harassment, increasingly prevalent in a world where everyone is online all the time. In 2020, 44% of all internet users in the U.S. said they have experienced online harassment. Social Media may have caused a lot of good in the world, but it has also caused harm in a way that arguably no other technology has caused in human history. Between 2007 and 2021, the suicide rate among Americans aged 10-24 rose by 62%, with the female rate between the ages of 15-24 rising by a staggering 87%. Meta is by far the world’s largest social media player and investing in this company should be viewed with an ethical question mark.

These questions about ethics have now caused countries to implement changes and bans that directly affect the Meta platforms. Australia has implemented a blanket ban on children under the age of 16 from using Meta which deactivated 4.7 million accounts within the first month. Other countries like Denmark, Spain, France and more are now looking at Australia to decide whether a ban like this is something they should implement as well. These bans could likely widen to the rest of the world and severely impact Meta’s user base and future revenues. In addition, governments have begun scrutinizing Meta much more closely. In 2025 Meta got hit with a €200 million fine from the EU. Meta was also hit with a $16 billion tax hit in Q3 of 2025 due to a change in the tax laws after the “One Big Beautiful Bill Act” passed stricter regulations on large corporations. These are only some of the first potential bans and fines implemented. As the negatives of social media become more and more apparent every day, governments will continue to look at Meta and big tech under a microscope and will likely take a more hardline approach against social media companies.

The Business:

Ever been scrolling through Instagram and suddenly come across an advertisement for a cool in style new sweater, right after you noticed your winter wardrobe looking empty? This isn’t by chance, Meta uses AI powered data from its 3.5+ billion users to tailor the perfect advertisements to each specific user. This investment has paid massive dividends and the Average Revenue Per User (ARPU) has skyrocketed from $27 in 2020 to $57 in 2025 boosted mostly by 28% gains over the last two years.

By testing many ad variations, AI matches each creative with the right audience, uncovering new customers marketers might otherwise miss.

Meta has also begun integrating and pushing its Meta Advantage+, its AI integration tool built directly into Meta’s Ad Manager. Meta has built a whole ecosystem that can run your ads for you from the beginning to the end. You can submit your product and Meta can manage your budget, build you an ad, find the people to send it to and distribute it all at a 9% lower cost per action on average. If you want it only to automate certain parts of the ads, you can do that as well, including taking your version of an ad and adding music, pictures or anything else you want. While currently not all users prefer Advantage+, Meta has now made it the default and is pushing users towards using their AI tools. These AI tools already objectively perform better than regular ads and have 22% higher returns than standard campaigns. Currently, most professionals still advise feeding a high quality product for the best results but in the future, Meta will likely be able to automate the whole process. For Meta, it’s a simple formula, better AI increases their productivity, which in turn increases revenue from ads which get reinvested back into AI and the company.

Meta has also barely begun to utilize one of its biggest assets. WhatsApp. WhatsApp boasts over 2.3 billion DAU and is currently totally free to use for the average user with limited advertisements. Even with that, Meta still manages to make significant revenue and in 2025, WhatsApp implemented a “Click-to-WhatsApp” feature which is used when a user clicks on an advertisement and gets directed to a chat which is used as a checkout. This format has proven significantly more effective than average website links and Meta therefore charges a premium for this feature. Meta has also introduced advertisements in the updates tab and while these are still far away from the personalized targeted ads on Facebook due to WhatsApp’s end to end encrypted nature, these will likely only improve and increase revenue in the future. In addition, WhatsApp charges larger companies per conversation and this revenue stream is projected to pull in $3.6 billion in 2026. These are only some of the new revenue streams that Meta has created using WhatsApp and likely in the future they will integrate more and more effective ads and revenue streams into WhatsApp.

The Financials:

Meta’s massive spending is likely one of the main reasons the stock is currently down 1% in the last year despite the market being up 18% - although the stock has had its volatility, climbing to almost $800 before falling back down to its current levels around $650. While investors believe in the platform, it’s hard to imagine how a company even as large as Meta can spend over $100 billion in one year and return the investment, especially as much of the infrastructure they are currently building will likely be outdated in a few years. Yet Meta believes that its spending is justified and during their last earnings call they announced $115-135 billion in CapEx for the upcoming year with the majority of those costs being driven by building infrastructure. However, even with this massive amount of spending Meta believes that its operating income (Gross Income - Operating Expenses) will actually increase in 2026 because of the effectiveness of AI spending.

It’s important to note that unlike Amazon (who hosts AWS services used by massive companies including Netflix, Amazon, Airbnb and more) or Google (who hosts Apple, Spotify, X [Twitter] and more) Meta’s CapEx spend is going directly back into improving their company and making advertising more efficient. In addition, Meta has made its LLM Llama open source, meaning anyone can access the code behind it and improve it as they see fit. Because Llama is completely free to use, developers will use it instead of a paid competitor and thus become more integrated into the Meta world. Finally, Meta is utilizing this massive spend in order to make sure that they won’t be beholden to anyone else when it comes to AI infrastructure and will be coming to the table from a place of strength rather than weakness. Meta is building data centers, establishing new partnerships and contracting cloud capacity all to make sure that Meta is in the best position moving forward.

We are now seeing a major AI acceleration. I expect 2026 to be a year where this wave accelerates even further on several fronts. We're starting to see agents really work. This will unlock the ability to build completely new products and transform how we work. - Mark Zuckerberg, Q4 Earnings Call 2025

Meta’s Revenue is fast accelerating passing the $200 billion in 2025. Over the past two years its average growth rate has increased by 22% a year, an impressive increase over an already fast growing 5 year average of 18%. If we assume that Meta’s growth rate slows to its five year average (despite indicators that it will increase rather than slow down) and assume a P/E multiple of 25 - slightly lower than the current P/E of 28 and relatively conservative for a tech company, you get 20% returns for the next five years. This may be why Bill Ackman, a hedge fund manager who manages $20 billion with a 321% return in the last ten years (narrowly beating out the S&P which has managed 308% returns,) opened up a brand new position in Meta worth 12% of his portfolio. Bill Ackman only buys stocks when he has a high conviction in them and his portfolio is famously concentrated with only 8 stocks making up over 97% of his portfolio. This is a stock that seems to be mispriced - at least according to its financials.

Meta seems to have a very strong future ahead and it’s investing heavily to make sure that it doesn’t fall behind in the AI race. With half the world’s population on their platform and AI advertisements that are improving at an extremely fast rate, the company is poised for massive growth going forward. So far, only Facebook and Instagram maximize Meta’s massive advertising potential and in the future, if Meta finds a way to properly advertise its products on WhatsApp and Threads, the revenue and stock could climb exponentially. The ethical concerns remain and are legitimate but if you are evaluating Meta purely as a business, it seems extremely healthy with no signs of slowing down.

Disclaimer: For those of you reading this, remember I’m sharing my personal journey and opinions, not professional investment picks.